A Practical Framework for ECIP Lenders and Their Borrowers

Community banks and CDFIs holding Emergency Capital Investment Program (ECIP) allocations are struggling to find the borrowers that the program was designed to reach.

Small manufacturers, minority-owned firms, family businesses, and first-time borrowers don’t usually walk into a bank asking for ECIP capital, don’t know these programs exist, or don’t have the experience or advisor relationships to complete complex applications.

Avalon Growth Capital’s framework focuses on three practical questions:

Where are ECIP-eligible businesses located?

What are the pre-qualification steps before credit evaluations?

What are long term support models to ensure effective capital placement?

The Capital Deployment Gap

Case Study: ECIP

Same principles apply to SSBCI, USDA Rural Development, CDFI Fund, EDA, State Programs

Traditional commercial lending expects a borrower with a need to walk in, so the bank can underwrite and close. That model works for businesses that already have institutional access. This likely will not work for the ECIP.

Most qualified applicants have never filed a commercial loan application or even know where to start.

ECIP alone represents over $9 billion for community banks and CDFIs. Across similar federal and state programs, more than $50 billion is available, however the most eligible borrowers are not coming through the door.

The missing link here is a strong system that can find, educate, and qualify the right businesses proactively - building a qualified pipeline for lending.

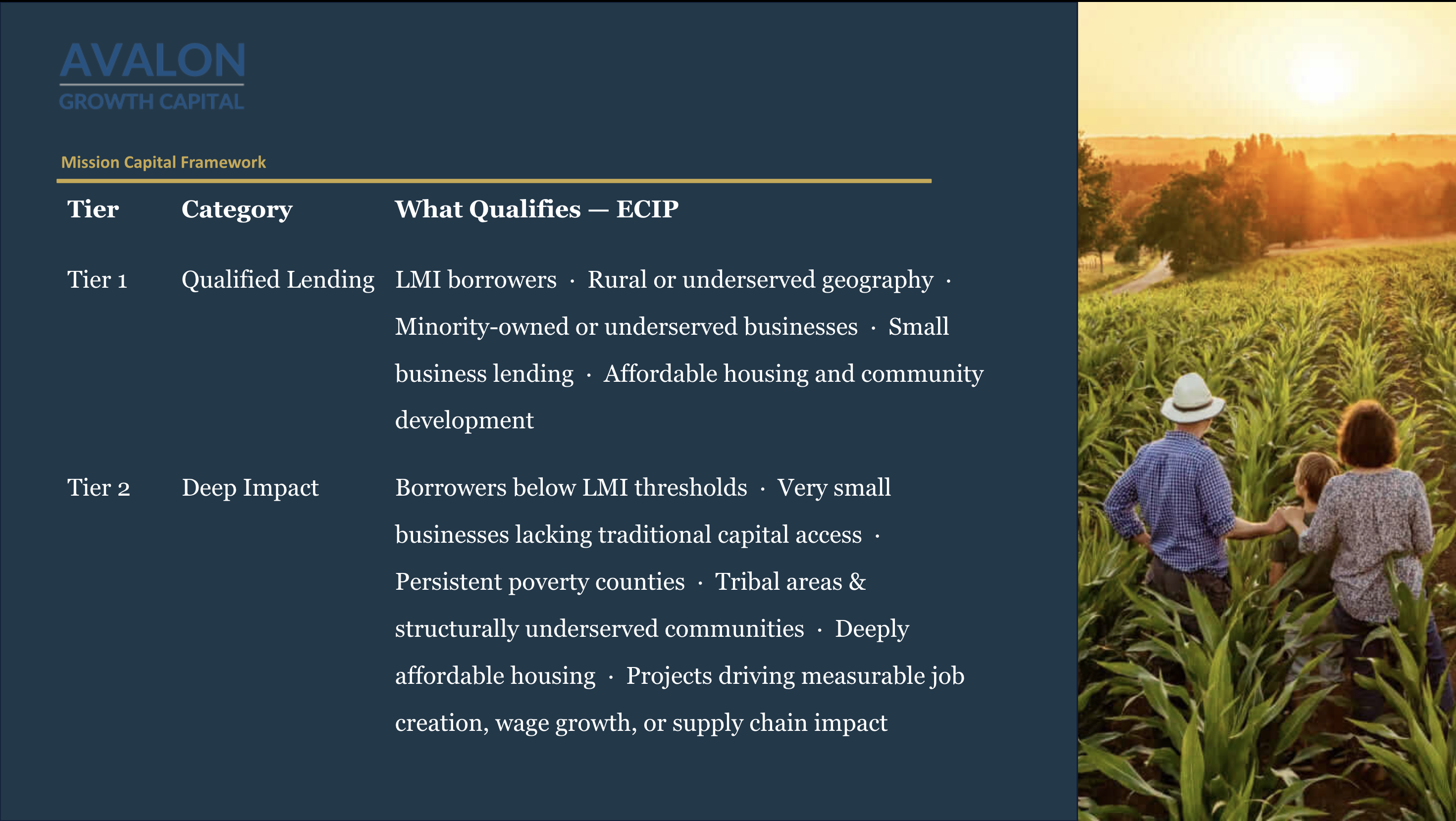

The Mission Capital Framework

Every mission capital program has its own eligibility rules, but they cluster around common dimensions:

Where the business is (geography, census tract, rural/urban, poverty level)

Who owns it (minority, women, socially disadvantaged, tribal, etc.)

How big it is (revenue, number of employees)

What it earns (borrower income/firm revenue vs. area median)

What impact it has (jobs, wages, local supply chain, underserved community)

ECIP’s Tier 1 and Tier 2 framework is the most detailed and instructive example of how these dimensions are operationalized.

Where the Deals Are

Five deal categories represent the most consistent and accessible sources of ECIP-eligible flow in rural and underserved markets. These same categories appear repeatedly across USDA, SSBCI, and CDFI Fund deployments.

Rural Ag Supply Chain

Beef processing, dairy, grain handling, cold storage. These businesses sit simultaneously in rural geography, persistent poverty counties, and supply chain impact categories that qualify strongly for Tier 2 classification.

Manufacturing with A/R & Inventory

$3M–$15M manufacturers in underserved markets often carry significant receivables. Traditional lenders often pass on unfamiliar collateral structures, but these deals qualify cleanly at Tier 1. Asset-based lending against A/R and inventory is also the fastest-closing structure in mission capital deployment.

Tribal Area Businesses

The most consistently ECIP-eligible category and the most underserved by advisory relationships, Tribal geography is an explicit Tier 2 qualifier. Historical exclusion from institutional capital means most operators meet the “lacking access” criterion automatically.

CDFI Capital Recycling

CDFIs that originated qualifying loans may need balance sheet relief for new opportunities, creating a secondary market for pre-qualified, mission-aligned assets — particularly in bridge structures ahead of USDA, HUD, or other federal program takeouts.

First-Time Capital Seekers

Operators who built real businesses in persistent poverty geographies without institutional support.

Pre-Qualification Before Presentation

Your credit and data teams move fastest when the presenting advisor has done the pre-qualification work beforehand. A well-prepared ECIP deal package includes:

Census tract designation, county poverty classification, and rural or underserved community confirmation with the data source cited.

Borrower income or revenue relative to applicable MFI and AMI thresholds.

Business description with years in operation, employee count, and capital access history.

Ownership structure and any minority, women-owned, or socially disadvantaged designation with supporting documentation.

A quantified impact narrative, such as specific job creation figures, wages relative to county median, supply chain relationships supported.

Full capital structure showing where the ECIP deployment fits the broader stack and proposed terms.

At minimum two years of financial statements or a credible projection with documented assumptions

Five Key Questions Every ECIP Deal Should Answer

1) What census tract is this business in, and what is the MFI or AMI designation for that geography?

2) What is the borrower’s income or revenue relative to the area median income threshold for LMI or low-income classification?

3) Does this deal qualify at Tier 1, and does any element of the profile, geography, or use of proceeds support a 2x impact classification?

4) What is the full capital structure, and where does our ECIP deployment fit within it? Who are the other lenders or investors?

5) How will this borrower meet ongoing impact reporting obligations post-close, and what support is in place to ensure compliance?

Capital Velocity - Deploying Funds

Lending institutions have several key objectives: Strong impact, efficient use, and recycling of capital. The following structures help to move ECIP capital quickly and productively by these principles:

Working Capital Lines Against A/R and Inventory

Manufacturers and distributors with steady receivables cycles can turn these lines in 90–120 days of active earning.

Bridge financing with a defined federal takeout

A community bank providing bridge capital ahead of a USDA, HUD, or similar federal program takeout can deploy ECIP for 12–24 months with a clear exit. The credit is underwritten against the quality of the underlying deal and the reliability of the takeout.

Debt refinancing with improved structure

Many ECIP-eligible businesses carry legacy debt from community lenders and refinancing with an ECIP-backed facility improves the borrower’s terms for capital. This also often qualifies for Tier 2 classification, since the existence of that legacy debt is evidence of the historical capital access gap.

Loan Participations and Syndications

An ECIP bank does not have to be the lead lender on every deal it touches. Loan participations between ECIP-participating institutions and other lenders, including non-CDFI community banks, let an institution put Qualified or Deep Impact dollars to work in geographies outside its branch footprint. Federal banking regulators have explicitly recognized loan participations with CDFIs, MDIs, and Low-Income Credit Unions as creditable community development activity under updated Community Reinvestment Act guidance, which makes the structure attractive to participating banks on both sides of the table.

Stacking with Federal Credit Enhancement Programs

ECIP capital pairs cleanly with USDA OneRD guarantees (Business and Industry, Community Facilities, REAP), USDA 9003 biorefinery guarantees, the BIA Indian Loan Guarantee Program, New Markets Tax Credits, and SBA programs. Stacking ECIP capital with a federal guarantee can lower risk on a deep impact transaction, increase the deal size a participating bank can absorb, and frequently brings a higher Qualified or Deep Impact classification within reach. For complex transactions in rural, tribal, or persistent-poverty geographies, this is often the structure that gets the deal from interest to close.

The Importance of Long-Term Support

For both the lender and the borrower, this is the beginning of a capital formation journey that requires ongoing financial support to execute effectively.

When a firm with credit discipline stays engaged, the likelihood of capital misallocation, operational drift, or reporting failure drops significantly.

The Continuity Value

For the originating institution

De-risked credit position. A borrower with ongoing financial advisory support is less likely to misallocate capital or fall behind on program reporting. The institution’s ECIP compliance record improves in proportion to how well its borrowers are managed after close.

For the borrower

Ongoing balance sheet optimization, capital structure review, and strategic guidance as the business scales. Founders who built their businesses operationally often need a financial partner thinking ahead of the next capital event while they run what they built.

For the program

Every mission capital program carries ongoing impact reporting obligations. An advisor who stays engaged ensures those obligations are met consistently, accurately, and on time — protecting the borrower’s standing and the institution’s compliance record with the agency.

For advisory firms with direct experience in ECIP and comparable programs, post-close engagement is the natural continuation of the origination and structuring work — the point where a transaction becomes a relationship, and where the most durable institutional partnerships are built.

A Prime Opportunity Profile

A Practical Starting Point

The quality of the support models and the advisory relationships in finding and supporting these businesses will play a critical role in extending the program benefits into the places where eligible deal flow actually lives.

Three things worth having in place:

1) A clear internal eligibility brief - This is a two-page document specifying your criteria in operational terms: target deal size, preferred geography, Tier 1 vs. Tier 2 priority, preferred structures, and documentation your credit team needs at first presentation.

2) A fast internal screening process - In order to deploy most efficiently, institutions must confirm eligibility fast and at high quality to earn trust.

3) A clear position on post-close advisory continuity - Decide before the first deal closes whether your institution expects borrowers to manage reporting obligations independently or whether advisory continuity is built into the relationship structure.

Avalon Supports Mission Capital

Avalon Growth Capital built its ECIP capability from the inside out — through direct origination experience in rural agricultural finance, persistent poverty markets, and asset-based lending structures that most advisory firms have never underwritten. That same depth extends to SSBCI, USDA rural development, CDFI Fund, and comparable state programs, because the underlying origination discipline transfers across every program built on similar eligibility logic.

Avalon Growth Capital is a boutique advisory firm working at the intersection of rural and agricultural finance, community development lending, and business transition advisory. The firm brings together credit discipline developed through decades of underwriting agricultural and community development deals from inside lending institutions, and the relationship capital that accumulates through years of working on both sides of the transaction.

Avalon’s advisory engagements range from debt capital formation and refinancing for production agriculture and manufacturing businesses, to sell-side advisory for founders navigating their first institutional sale process, to long-term retained advisory for clients requiring ongoing financial strategy, capital structure support, and program compliance — and institutional deal flow sourcing and pre-qualification services for ECIP-deploying banks and mission-driven fund managers across the Plains, Mountain West, and Southeast.

Recommended for you

Avalon Growth Capital Shares Insights For Sourcing Mission-focused Deal Flow in Rural America

Avalon Growth Capital Shares Learnings on Fund Formation and the Capital Raising Process

A Grant Writing Case Study: The U.S. Forest Service Wood Innovations Grant Program

We are driven by a passion to transform the world by empowering visionary entrepreneurs who dare to challenge and redefine today’s standards.

Partner with us

Let’s talk about the future growth of your business

Partner with usConnect with us to discover how our customized business consulting and investment banking advisory services can benefit your business.

.svg)